USDX has held (so far) at 78.60, Gold tops out at $1777 and EurUsd hits 1.3170 but US T- bonds look like they have found support on my LMLP ( see previous posts).

An endless open committment for $40 bill a month and all so far is about 40 big points on the emini S&P

. All we need now to evaporate that is a pre emptive strike by Israel on Iran (and there are current rumours in diplomatic/political circles that this is on the cards before the US pressi elections) and we may end up back where we started or lower.So what does the next few months hold in store? How on earth will the Feds action whereby it buys from banks/institutions who then reinvest in stocks or other asset classes effect the average man on main street USA and create wealth... Understanding and getting ones head round the macro economic effect of recent monetary policy is difficult for me perosnally but I do agree that a large rally in stocks does not seem a rational outcome since we are already 37% higher since a year ago ( $SPX) but then markets are simply not rational and no longer seem correlated to the wider world and economy and are ostensibly driven by cash rich banks/institutions with eye watering amounts of cash to pump around various asset classes. Here is a most encouraging appraisal of the current situation Why QE3 cant work by Joseph Stuber reproduced here without permission ( ooops!sorry) from Seeking alpha.( link at bottom of page)...It all makes perfect sense however i for one am not considering shorting the S&P and if anything expect to see 1500 rather than 1400 by Xmas 2012

The bottom line and my final word (today!) on this subject ( the words below are of course by Joseph Stuber) is that if it looks like a rising market, smells like a rising market, feels like a rising market then......it is a rising market and bollocks to the marco point of view -I will buy any significant retracements and especially if fundamentals cause a volatile sudden dropfrom euro concerns or Israeli 'projects' etc.

http://seekingalpha.com/article/869461-why-qe3-can-t-work-understanding-the-liquidity-trap

Why QE3 Can't Work: Understanding The Liquidity Trap by Joseph Stuber

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More...)

The Fed's move on Thursday to a massive and open ended

injection of money into the U.S. economy certainly had an impact in the

short term as traders tried to assess the significance of this new QE

initiative. It pushed stocks higher and bonds lower in a rather dramatic

knee jerk reaction to the announcement on Thursday. How effective the

plan will be over time is a matter for careful consideration.

The

markets had moved 8% to 12% higher - depending on the stock or the

indices one looks at - over the last 6 weeks. Another percent or two was

added Thursday after the Fed's new QE - an open ended bond buying

program of unprecedented size - was announced. As a trader I admit to a

moment of hesitation as I tried to process the impact. I monitored the

stock indices but kept glancing over to bond yields, the metals and

crude.

What caused me some degree of confusion was the movement in

the bond market. The short end of the curve was falling and the long

end rising. The Fed's new program wasn't a sterilized purchase like

Twist - we were creating new money here - so the short end of the curve

falling didn't make sense. Even more confusing was the long end of the

curve. Traders were selling bonds and selling them hard. Why? With the

Fed committing to buying mortgage backed securities in large quantities

the long end of the curve should be stable or falling I reasoned.

I'm

not a bond trader and admit that I don't have all the answers but the

movement didn't make sense to me. There was something I wasn't

processing about all this. I jumped on the Federal Reserve website and

read the statement. It seemed a little ambiguous. I wasn't sure if the

plan was to buy the bonds on the open market or if the purchases were a

normal QE designed to add additional liquidity to the banking system.

It

was important to me to know the answers to these questions. I have done

a lot of research on QE's impact to the relevant metrics over the last

several years and a program designed to add liquidity to the banking

system in my opinion was a non-event as we have been stuck in a

liquidity trap since the Fed began QE. The proceeds from those purchases

would end up being trapped money - setting on the balance sheets of

banks and doing nothing.

On the other hand, if the purchases were

going to occur outside the banking system then the impact would be more

significant. $480 billion a year injected into the economy is huge -

almost 3% of GDP. That would be new money and would leave the total

money supply flat even after the "fiscal cliff" tax hikes and spending

cuts occurred. The Congressional Budget Office has projected the deficit

to be reduced by about $500 billion next year and the Fed was

effectively making the impact of the tax increases and spending cuts a

non-event - at least from a macro point of view.

I admit to still

being a bit confused as to how this new money will impact GDP but for

the moment at least I have decided that most of the new money would

likely flow directly into the stock market. The aggressive selling of

bonds along the long end of the curve suggests to me that these bond

holders are dumping bonds and planning to move to stocks and metals

anticipating ramped up inflation. There is really no other reason that I

can come up with to explain why long bond yields would climb when we

already know the Fed has every intention of holding yields down on the

long end of the curve.

This is significant in that the Fed's money

for these purchases will likely go to banks or institutional investors

and therefore be reinvested. If my logic is sound the impact will be

diminished as the velocity of this new money will be comparatively low.

The Fed buys the securities from a seller - the seller takes the money

and buys stock or another asset and that is that.

Perhaps I'm

missing something but I'm pretty sure what's needed is to break free

from the liquidity trap we are stuck in due to fear and uncertainty and

driving stocks and metals higher will not achieve that end. As an

analyst, this new QE has increased my fear and uncertainty - not reduced

it.

If all that's happening here is that the Fed buys agency

securities from institutional investors and banks and the institutional

investors and banks in turn buy stocks or gold it will add a modest

amount of upward pressure to the price of stocks and gold. It certainly

won't flow into the broader economy where the velocity of this money

could work to spur significant GDP growth.

$40 billion a month is

relatively insignificant considering the total capitalization of all

publicly traded companies is in excess of $50 trillion. The possibility

is real that these funds will work to drive stock prices higher if the

trend is higher to begin with but the dollar amount is probably not

enough to significantly alter normal market action or direction. High

frequency trading algorithms will absorb and overwhelm the volume

created by the Fed's action.

In the end I decided we were still

dealing with a liquidity trap. For the Fed's plan to work and break us

out of the liquidity trap we are going to need more than a stock market

rally. If the market response to the Fed action on stocks and bonds

translates to a similar reaction on the part of local banks and

consumers the plan will work. If consumers react with more disgust and

more fear the plan will fail. It is really that simple.

Perception Must Precede Fact For The Plan To Work

The

Fed's plan - although they deny it - is to induce an inflationary

environment. Perception precedes fact in this instance. If public

perception is that we are entering a period of high inflation two things

will happen:

- Bank lending will increase

- Consumer borrowing and spending will increase

As

massive as the Fed's move is from a historical perspective - if my

analysis is correct - it will have minimal effect on the broad economy

as the money won't flow into the broad economy. Additionally the

velocity of this money will be nil since it won't flow into the hands of

the broad population where it would be used over and over again as

people buy and sell with the money driving GDP.

That leaves the

Fed action impotent unless it works to change Main Street's perception

of what's to come. That seems doubtful. Notwithstanding the fact that

this is a move of huge proportions - a "shock and awe" move - it is

doubtful the public will recognize this fact or even care. If not, it is

a "dead horse" strategy and you can't win the race on a "dead horse".

There

is very little empirical evidence to support quantitative easing as a

legitimate strategy to affect the desired result. Japan's experiment

with quantitative easing is perceived as a failure and critics are quick

to point this out. As Bernanke readily admits in speeches and

statements the Fed is learning on the fly as evidence of non-traditional

policy impact is limited.

Ben Bernanke's legacy is clearly on the

line. Prior to the Fed's announcement I speculated on the odds of a new

round of QE and discounted the possibility setting the odds of QE3 at

zero - a rather bold and ridiculous assessment on my part in retrospect.

My logic was that additional QE would not manage to stimulate bank

lending or motivate consumers to shift from a cash hoarding mindset to a

free spending mindset.

As a part of my analysis that led me to

conclude that the Fed would stand pat I did consider the possibility

that the Fed had two choices - do nothing at this point or enter into a

massive "shock and awe" stimulus plan. The second choice is wrought with

risk. My thinking led me to the conclusion that now was not the time to

take big risks. It is the Fed's last bullet in their policy gun. If it

fails Bernanke's legacy goes down in the history books as an abysmal

failure.

We may not know for some time how the Fed's "shock and

awe" stimulus will translate in the broad economy but we can at least

look at where we are and attempt to speculate on what the Fed's policy

move will mean. I don't think it is logical to give Bernanke a passing

grade at this point. This unprecedented move is analogous to being down 3

runs in the bottom of the ninth with the bases loaded and the batter

down in the count 2 strikes. Anything less than a homerun is meaningless

- the game is lost.

Liquidity Trap

Real

economic growth must be built on the backs of the consumer. When

consumers hoard cash out of fear no economic expansion will occur

regardless of monetary policy.

Karen Murdarsi, in her article, "

Keynes and the Liquidity Trap", explains in an easy to understand way what Keynes meant by liquidity trap:

Why

did Keynes believe that government spending was the way to break the

cycle? To answer that we need to look at the other ways of controlling

the economy.

1) The government (or the central bank) can

try to reduce the 'price' of money by lowering interest rates. The laws

of supply and demand say that low demand reduces the price of goods to a

level where people want to buy them. In the case of money that would

mean reducing the cost of borrowing, i.e. interest rates. The trouble is

that in a recession, people may be so unwilling to borrow and invest

that it is impossible to reduce the price far enough. Once interest is

at zero, there's nowhere else to go.

2) The government

(or bank) could increase the money supply - they could literally (or

electronically) print more money. The idea is that this money will work

its way around the economy, allowing people to spend and invest more,

and increasing employment. The trouble is that when times are bad people

want to hold on to their money. They don't want to invest it in stocks

which might fail, or spend money on goods and services when they fear it

will leave them short later. They feel safer holding on to money in

'liquid' form (CASH) which means that all the new money released is

hoarded by nervous banks and savers, and does nothing for the wider

economy. This is what Keynes identified as "the liquidity trap".

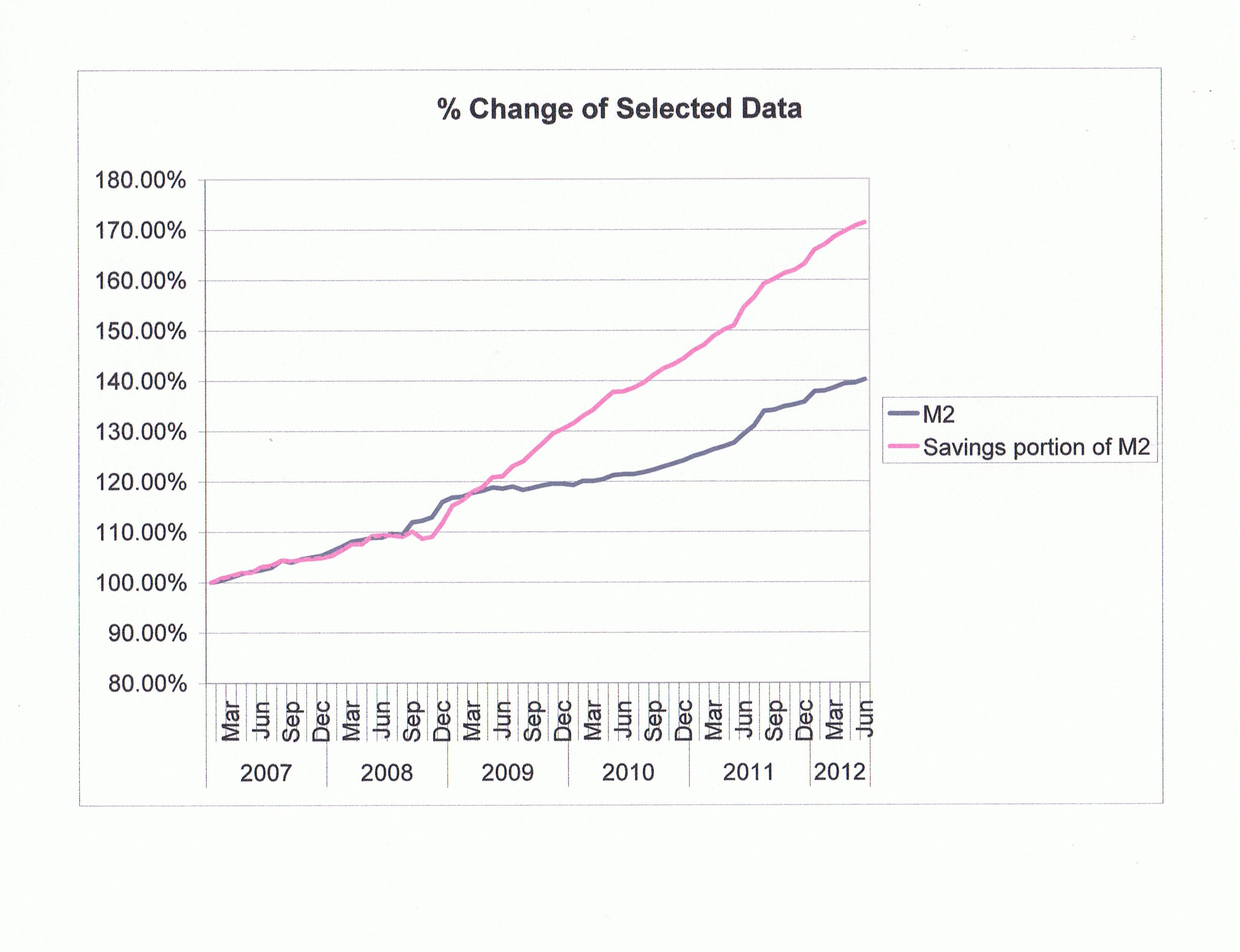

The

chart below clearly shows that through QE1, QE2 and Twist America's

recovery has been stuck in a liquidity trap. What is particularly

interesting about this chart is that M2 and the Saving component of M2

were closely correlated from the beginning of 2007 until the Fed started

QE1 in November of 2008. From that point forward the Savings portion of

M2 moves higher at a much faster rate.

click to enlarge images

Perhaps

we cannot conclude with certainty that the Fed's QE programs were the

motivation behind our sudden propensity to save. What we can conclude

with absolute certainty is that the Fed's QE programs did nothing to

quell our fear since American's started a process of systematic savings

that has continued without a slowdown from the time QE began until the

present.

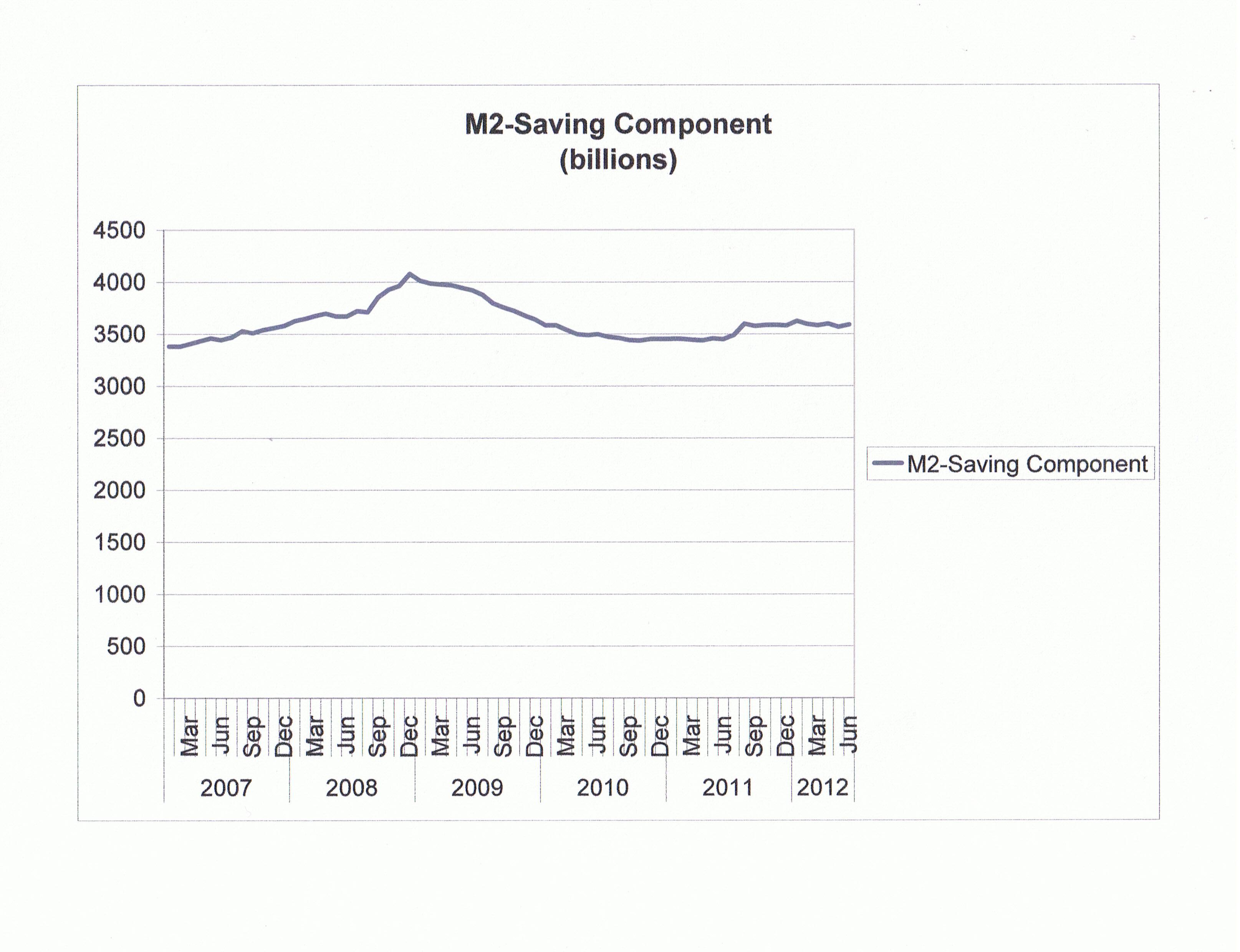

The next chart shows the real impact of the liquidity

trap. This chart shows the spendable cash in the economy - cash that

drives GDP growth. Spendable cash is calculated by subtracting the

Savings component from M2. Take note of the fact that real spendable

cash actually fell from $3.963 trillion in November, 2008 to $3.589

trillion today.

Looking

at just this single metric it is clear that monetary expansion has not

achieved its intended result. The Fed's balance sheet has increased by

approximately $3 trillion since they started QE. Almost all of that went

into savings - not into the general economy where its effects would be

multiplied as it moved from one hand to the other. Money velocity has a

multiplier effect on GDP growth. As money changes hands it is spent

again and again the result being a single dollar might translate to $5

or even $10 in GDP.

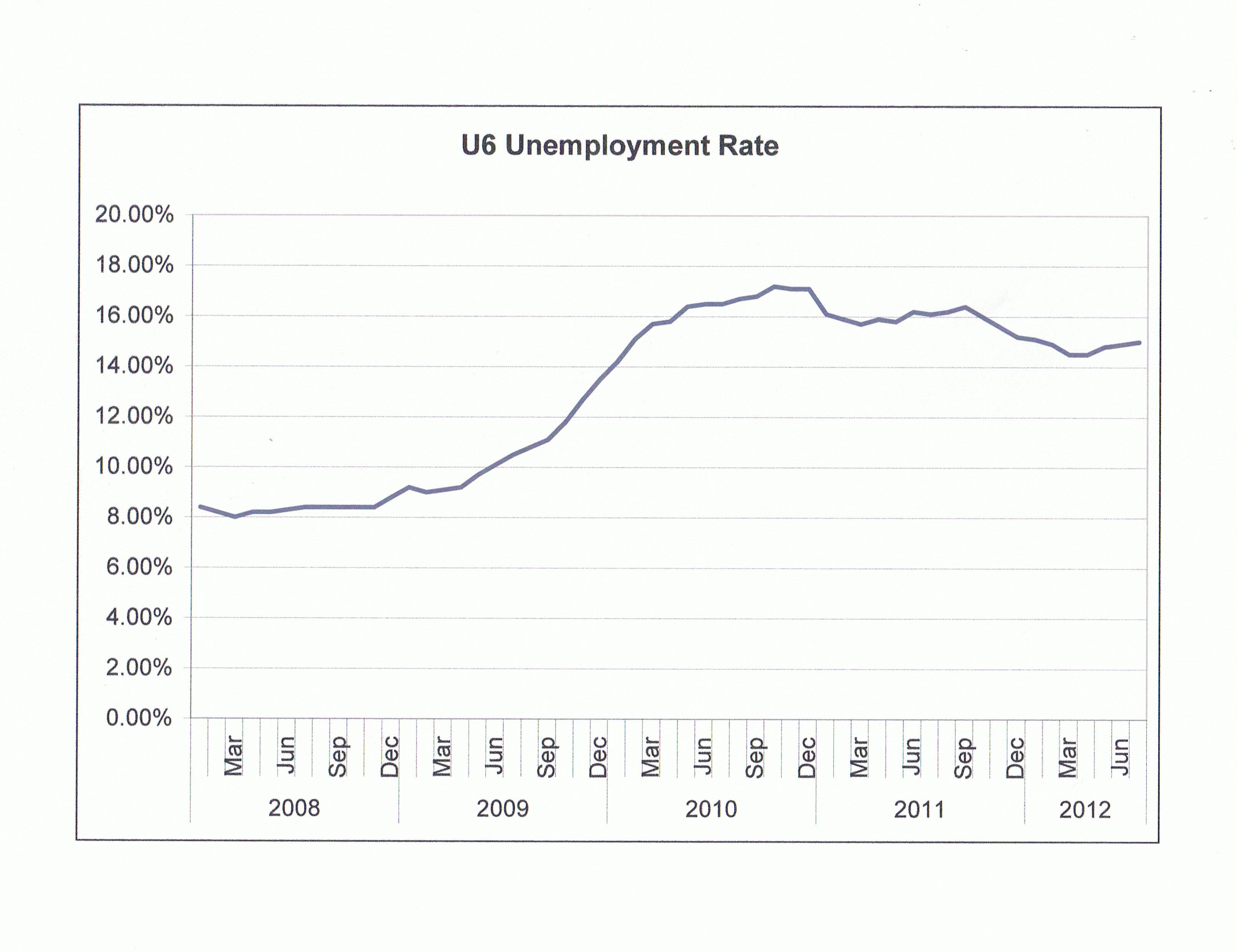

Let's look at another metric - unemployment.

There is a very strong correlation between the chart above reflecting

the reduction in spendable money supply - resulting from an increase in

the rate of saving - and the U6 Unemployment Rate. Spendable income

peaked and started its descent in the 1st quarter of 2009 at the same

time that U6 unemployment rate started its climb.

Without

an increase in spendable money GDP can't grow and without GDP growth

unemployment can't fall. Let's look at another metric - GDP growth:

The

chart above shows real GDP growth and inflation adjusted GDP growth.

After accounting for inflation there has been no growth in the economy

at all. This has to be a huge disappointment for Bernanke.

The

take away from all this is that for the new "shock and awe" plan to have

it's intended effect we have got to break free from the fear and

uncertainty that has gripped the nation since the recession. To date we

have made no progress at all in any of the major metrics that we look

at. As Keynes states:

".. if

Investment exceeds Saving, there will be inflation. If Saving exceeds

Investment there will be recession. One implication of this is that, in

the midst of an economic depression, the correct course of action should

be to encourage spending and discourage saving. This runs contrary to

the prevailing wisdom, which says that thrift is required in hard times.

In Keynes's words, 'For the engine which drives Enterprise is not

Thrift, but Profit."

Where's The Market Going From Here?

From

a trader or an investor's perspective what we need to figure out is

whether or not we should ride the "Bernanke bull" or get off now. It's

been a nice ride for the last several weeks but can it continue.

My

conclusion is that even under the best scenario - a massive increase in

inflation - we have probably priced in the full effect. In other words

if the Fed's plan works to raise inflation to maybe 4% - which is in my

opinion the outside limit of inflation expectations even if the Fed

policy does shift consumer sentiment - that and more is already priced

into the market.

We can momentarily get caught up in the euphoria

but really how high can we expect the market to go on the backs of even

an overwhelmingly successful outcome where the public jumps in with both

feet and starts borrowing and buying with frenzy? Consider that the

October low on the spot month S&P 500 futures contract was 1068.

Friday's close was 1465 - a 37% increase. There is no way inflation can

support that kind of move.

You can argue that the October low was

not reflective of the real economy if you want and therefore the 37%

move in the market is more reflective of reality. I would take the

opposite side of that argument and offer up the following facts as

support for my argument:

- Depression era unemployment numbers.

- Flat GDP growth.

- Liquidity trap that is locking up all Fed stimulus money.

- Pending fiscal cliff issues.

- Eurozone recession.

- China contraction.

- Record debt to GDP ratio.

- Failed monetary policy.

That's

a short list. If the S&P were at the bottom end of the 12 year

trading range I might be a little more positive but we are not. We are

at pre-recession highs and a comparison of economic metrics today versus

when we were at these price levels pre-recession provides a shocking

contrast in economic health.

I have said we are our own worst

enemy as it is only through the collective population's increased

confidence that we will start to borrow and spend. The Fed hasn't

provided that confidence with their policy moves. On the fiscal side it

is the same thing. "We the people" just aren't buying and without us no

policy move matters. As long as fear and uncertainty permeate the minds

of the people they will be prudent and cautious. As long as that

continues we will continue to stagnate as an economy.

Monetary and

fiscal policy - had it worked - would have made sense. It hasn't worked

leaving us in a far worse position than before these massive stimulus

initiatives. Now we are dealing with the added problem of credit

downgrades. As bond prices begin to reflect in the downgrades and they

will, we have the added burden of a dramatic increase in carrying costs

on these huge debts.

In conclusion, I think Ben Bernanke goes down

in infamy as the one who created the monetary policy stock bubble of

2012. When will the market bubble finally pop? That's anybody's guess.

My guess is this coming week. There is no rational justification for

stocks adding on to a 37% gain in a year. Even if one sees the Fed

policy as positive the market has already discounted the perceived

success of the policy.

http://seekingalpha.com/article/869461-why-qe3-can-t-work-understanding-the-liquidity-trap

US T-Bonds

ES U12

Gold

{kind=link}